Age comes with a lot of things such as wisdom. Unfortunately, it also comes with some forgetfulness. Fortunately, there are things you can do to keep the brain sharp, small daily habits which can reduce the risk of cognitive decline.

Business & Estate Planning

Age comes with a lot of things such as wisdom. Unfortunately, it also comes with some forgetfulness. Fortunately, there are things you can do to keep the brain sharp, small daily habits which can reduce the risk of cognitive decline.

Exercise is one such daily habit. It increases blood flow, and thus oxygen to the brain; it also protects brain cells against destructive chemicals in the environment. Exercise also supports the production of new brain cells. Furthermore, research in the 2000s showed a relationship between cardiovascular risk factors and Alzheimer’s. Anything which can impair blood flow can cause strokes leading to cognitive decline, otherwise known as vascular dementia. The same activities that one would consider as beneficial to the heart, such as regular exercise, can therefore also be effective in protecting the brain. And, of course, there are other benefits to exercising regularly: it helps with energy levels, decreases anxiety and depression, and can help with sleep.

Sleep is another factor to maintaining a healthy mind. But as many as half of adults 60 and older are affected by insomnia, which can result in memory loss, depression, and other symptoms. It’s important, then, to pay attention to sleep hygiene and sleep schedules to ensure sufficient duration and quality. If it takes more than 45 minutes to fall asleep, or you have trouble staying asleep, it may be worth looking into treatment.

Eating well is another way to protect the mind. It’s important to ensure you’re getting enough vitamins A, B, C, D, E, folic acid and niacin. The USDA and the HHS describe two eating plans: the USDA food patterns or the DASH Eating Plan. Foods like nuts, fish, and wine have also been linked to a healthy brain.

Art, music, reading, writing, learning, and puzzles… these are also good for keeping the brain sharp. Art has been used as an Alzheimer’s treatment and to restore memory; and arts maintain and improve dexterity and fine motor skills! Adult coloring books have become popular in recent years, and can be found in many stores and online; watercolors and pastels are also relaxing. Meanwhile, music has been linked to improved memory and cognition, and can both elevate your mood and lower blood pressure. Learning and intellectual challenges like puzzles exercise the brain and improve its capacity. Mental exercise is thought to maintain and stimulate brain cells. This includes pursuit of hobby, learning new skills, using brain training apps, or taking on other new kinds of projects at work.

Read more at:

Having a child that has special needs comes with many challenges. One of the toughest challenges faced by many parents is knowing how to best care for their special needs child as they reach adulthood. There are many areas that need consideration when planning for the transition of a special needs child to adulthood. Let’s take a look at some of these areas.

Education

During childhood, the public education system provides for the bulk of the care, structure, and services that a special needs child requires. However, once they are out of public education, this support and service abruptly come to an end. If parents don’t plan for this transition, it can be difficult for the child and the family. That is why the Individuals with Disabilities Education Act (IDEA) requires that at age 14, the student’s Individualized Education Plan (IEP) contain a plan with steps that will be taken to help the special needs student acquire skills that are necessary to transition from school to the workforce. Schools are required to monitor progress of the students as they acquire the specific skills. It is important for parents to understand their child’s rights and for parents of children with special needs to be advocates for their child as they turn 14 and enter this time of transition.

Employment

Special needs individuals if trained in skills specific to the workforce can find ways to have a job. For example, the local Walmart hired a young lady who has special needs to work as a cashier. The young lady while in school had an IEP. From the time the young lady was in elementary school, part of her IEP include life skills goals. These goals allowed her to learn necessary skills to get and keep a job as a cashier.

Beyond preparing your child early for the workforce, it is helpful to research companies that hire people with special needs and determine the types of skills they will need to succeed. Then, parents or other caregivers, should seek out ways to develop those necessary skills in their child. The key to employment is being prepared to help your child both during and after school. Be patient with the process. Sometimes it takes time for a special needs adult to get hired. Many special needs people do not work because they are scared that they may lose benefits if they work.

Financial

Working can be a great way for special needs adults to earn some additional income. However, it is important to keep in mind that there are limits on the amount of money a special needs person can earn without affecting Social Security Insurance (SSI) and Social Security Disability Insurance (SSDI). Once a child reaches 18, these benefits are based on his or her own assets. Other ways to protect the assets of your special needs child is by creating a first or third-party trust. This way, your special needs child can draw benefits while also having assets.

If you are the parent of a special needs child, it is important to begin planning early for the future of your child. Don’t wait until your child is 18. The public education system can be a great resource but you will need to do some planning on your own. The good news is there are organizations that can help you and your child find the right employment opportunities to match their skills. An elder law attorney who specializes in adults with special needs can be very helpful in planning for the financial future of your child with special needs.

If you have any questions about something you have read or would like additional information, please feel free to contact us. Please contact our office at (212) 937-8420.

Moving at a fast breakneck pace, is the revolution of smart personal assistants. It took approximately 30 years for the cellular telephone to begin outnumbering people on the planet, but smart personal assistants are projected to outnumber humans in half of that amount of time by 2021. The technology-research firm Canalys expects 100 million smart speakers (smart personal assistants) will be installed worldwide by the beginning of 2020 and also estimates the number of smart assistant compatible devices will reach 1.6 billion in the US that same year. The numbers are staggering.

It is precisely because of these numbers that manufacturers of smart personal assistants like Amazon, Google, Microsoft, and Apple are pushing sales of their devices. Not only does a smart personal assistant allow for corporate monetization post-purchase from user data collection it is on the forefront of taking over your everyday space whether that be your home, car, or office. The corporation that garners the biggest market share with their smart assistant technology will lock in app developers, appliance manufacturers, and consumers into their company’s proprietary platform also called the ecosystem which ensures frictionless interoperability. Home automation and lighting is forecast to make up 49 percent of the market segment, followed by home security and surveillance (18 percent), audio and video entertainment (13 percent) and “other” appliance segment (20 percent).

The smart assistant with its voice technology is a significant boon to US seniors as more baby boomers are opting to age in place and smart voice technology simplifies remaining at home. There are the obvious uses for a smart assistant like calendaring events, medication reminders, home environmental controls, age-appropriate learning activities, and much more. Some of the newer applications of voice technology are pushing smart personal assistants into newer realms like digital therapist, companion, and caregiver. For the senior who is living at home and alone, these are wonderful new developments.

Research in the field of prosody, the patterns of stress and intonation in a language, are making smart assistants capable of detecting depression, loneliness, anxiety, joy, and anger to name a few. Initial research of emotion enabled artificial intelligence focused on emotion detection through facial expressions but quickly turned to the spoken word. Vocal signatures carry an incredible array of information from how you string the words in a sentence together, to tone, depth, rhythm, pitch, resonance, pronunciation, tempo, and more. These vocal features are then analyzed to suggest a person’s mood and subsequent best action practice for the senior.

The practical applications of this technology are numerous. A medical doctor with a smart personal assistant in their office can more readily pick up on identifiers that suggest patient depression. A smart car speaker in a semi-autonomous car can make informed judgments about the safety of handing over the controls to the driver based on vocal characteristics indicating stress or confusion. A smart personal assistant might pick up on loneliness in a stay at home senior and offer suggestions of music or other activities to engage the senior and lift their spirits. The smart personal assistant is also “someone” an elderly person can tell their troubles to without shame, recrimination or judgment. The smart assistant is programmed so that it never gets tired, never becomes distracted or bored with the content of “its person.” It is a bit like a therapist allowing the senior to get out all of their frustrations about growing old and losing their physical and cognitive abilities; even expressing fears for their future.

While smart personal assistant technology is currently not able to provide all of the benefits of a professionally trained human caregiver, therapist, or companion it is readily available, overall inexpensive, and can help alleviate the problems of too many seniors with too few attainable human caregivers to meet their needs. The technology may also outpace its human counterpart in the not too distant future if current research and development is any indication of success. The market forces for profit will continue to drive the expansion of the smart personal assistant and its associated products allowing for newer market segments and more importantly the ability for stay at home seniors to live their best quality of life.

If you have questions about what you have read, please don’t hesitate to reach out. Please contact our office at (212) 937-8420.

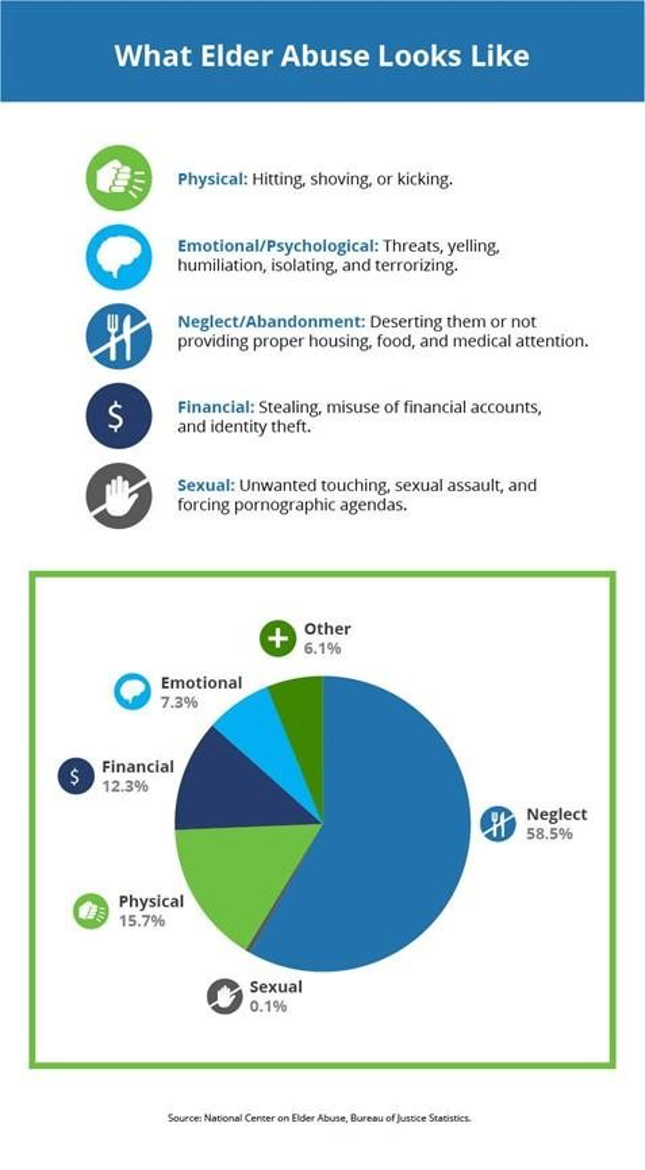

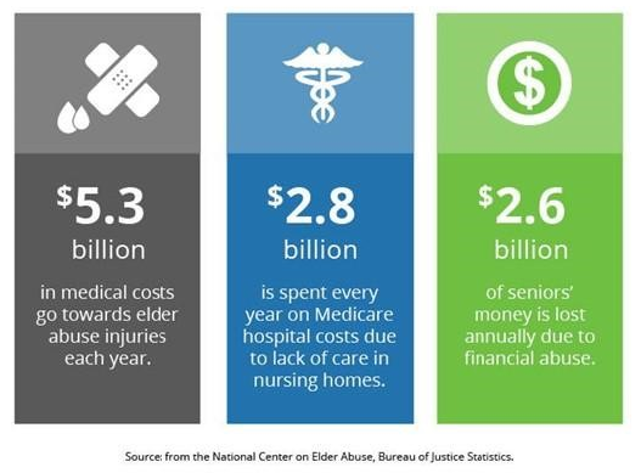

Elder abuse can vary and look different to different people. It may present itself in older adults’ lives concurrently. Sadly, elder abuse events are significantly underreported. The National Council on Aging reports that estimates range as high as five million older adults experience abuse every year or about one in ten. A study by The National Institutes of Health (NIH) estimates that only one in fourteen cases are reported to authorities. The number of abuse cases is increasing during the coronavirus pandemic as family and caretakers struggle under the strain of uncertainty and pressures of survival. Fully two-thirds of perpetrators of violence against elders are adult children or spouses.

Abuse includes physical, emotional, psychological, financial, or sexual abuse, and neglect or abandonment. The impact of the abuse comprises a host of issues in the elderly, including:

These underlying biological, social, financial, and psychological vulnerabilities are magnified as elderly individuals are disproportionately affected by social distancing policies and other restrictions to stop the spread of COVID-19. The loss of an elder’s social network makes it easier for an abuser to escape having their behavior cross-referenced by others. Caregiver and relative abuse indicators include:

Collectively, as a nation, negative attitudes pose significant risks to older adults’ health and well-being. For example, on social media platforms, the hashtag #BoomerRemover is trending and often is accompanying disparaging and devaluing memes. During the pandemic, public discourse increasingly portrays Americans over the age of 70, even 65, as frail, helpless, and unable to contribute to society. Since the coronavirus pandemic’s start, a massive increase in elder abuse reports occurs. Still, the abuse is probably being underreported. Family violence, financial scams, and neglect are heightened by the pressures all Americans feel due to coronavirus.

Adult Protection Services (APS) are available to victims of abuse or suspected abuse and are run by local or state health departments. While these agencies and departments investigate elder abuse, fewer financial resources are chasing increasing abuse cases. There is also insufficient access to data needed to resolve issues, inadequate administrative systems, and a lack of cross-training with the other agencies and disciplines in the aging field who serve clients, some with mental health disabilities.

Two of the more important federal acts that address elder abuse are the Older Americans Act (OAA) and the Elder Justice Act (EJA). Yet, these acts’ effectiveness has been diluted with a lack of funding and relaxed enforcement. According to Forbes, the EJA has less than 10 percent of the funding it was authorized to receive, and one of EJA’s main goals is to dedicate funding to Adult Protective Services. Underreporting, denial of, and underfunding of acts designed to protect older Americans from elder abuse is a significant problem in enforcing existing laws. Policy change requirements are needed to increase the protection of the elderly from abuse during the coronavirus pandemic and beyond.

Since help to identify and prevent elder abuse can be difficult to come by, older adults can employ several actions to reduce their risk of being victimized. To stay safe, it is important to:

Elder abuse is a criminal, civil, and moral offense. Victims vary by age, gender, background, and status, and the abuse can be domestic or institutional. There are ways to protect yourself or a loved one from financial abuse or fraud. If you have questions or would like to discuss how to mitigate the risk of elder abuse or fraud through legal planning, please don’t hesitate to reach out. Please contact our office or give us a call at (212) 937-8420.

Many health systems and hospitals have been coping with unprecedented challenges during the coronavirus pandemic of 2020. There has been a need to increase and safeguard healthcare staff as well as non-COVID-19 patients, testing and treating infected patients, expanding critical care unit capacity, procuring personal protective equipment (PPE), and canceling non-emergency patient procedures. The American Hospital Association estimates that healthcare systems are losing an average of 50.7 billion dollars a month. This financial crisis is jeopardizing the telehealth industry as insurance groups seek to lower rates for virtual appointments. Without payment parity equivalent to an in-person appointment, many health care systems will be unable to continue telehealth services.

COVID-19 has brought telehealth from a niche service to a common practice in less than a year. The assurance of physical distance, preservation of PPE, and limiting infection spread has been invaluable. Yet, despite the advantages telehealth provides, insurance coverage, prescribing, and technology access remain limiting factors. The federal government created the Coronavirus Aid, Relief and Economic Security Act (CARES Act) to address these concerns, removing many barriers to promoting telehealth expansion. The Centers for Medicare and Medicaid (CMS) created a toolkit to encourage state Medicaid agencies to adopts CARES Act standards, and many private insurers followed suit. Still, telehealth’s subsequent explosive increase in patients became unprofitable. The resulting financial strain on the healthcare system and insurers may force telehealth provision limitations, although the public health crisis remains.

Early in 2020, the use of telehealth saw an increase from 13,000 to 1.7 million Medicare recipient visits per week. During the height of the national lockdown, between mid-March to mid-June, the number of Medicare recipients receiving telehealth care was more than nine million. Meanwhile, private insurers, mimicking the CARES Act policy changes, saw telehealth claims increasing upward of 4,000 percent from 2019. The CARES Act intended to last until the public health emergency was over. With the advent of this flu season and the possibility of a second wave of coronavirus, there is a call for telehealth’s expansion to become permanent.

However, many private insurers are changing their telehealth coverage policies for non-COVID-19 issues due to financial losses. United Healthcare will no longer waive co-pays and other fees for non-COVID related appointments. Other insurers like Anthem BlueCross BlueShield will extend coverage through the end of 2020; however, only the first two telehealth sessions will be free for the consumer. Telehealth billing standardization remains elusive as each private insurance plan, and many state-funded Medicaid plans have varying rules and dates for what telehealth treatments have coverage. Some patients are paying more, while others are paying less. Costs are confusing, and patients may be delaying healthcare to avoid a surprisingly expensive bill.

America’s Health Insurance Plans (AHIP) is a trade, and political advocacy association of health insurance companies with certifications for Medicare Advantage and other CMS governed health plans. Working with public and private sectors, AHIP implements solutions to lower out-of-pocket costs, which can be a barrier for people seeking telehealth medical care. AHIP’s website lists many insurance providers and general information about their coverage, often addressing telehealth. If you or a loved one requires telehealth coverage, it is the optimal time to review your health care coverage for 2021 as the insurance industry is in its annual enrollment program.

Diminishing coverage for telehealth visits will continue to impact Americans this winter and beyond. Patients are paying more while health care practices are earning less, and the risk of infections increases. Health insurers seem to be driving patients back to the in-person appointment model. Telehealth is truly innovative and protective during the coronavirus pandemic, but its continuation will suffer unless it can also become profitable.

We hope you found this article helpful. If you have questions or would like to discuss a personal legal matter, don’t hesitate to reach out. Please contact our office at (212) 937-8420

Polling shows that the number one worry for Americans as they age is memory loss, outpacing fears of insufficient monies, and loneliness. The most prevalent among all dementia is Alzheimer’s disease. According to the Alzheimer’s Association Facts and Figures Report, Alzheimer’s accounts for an estimated 60 to 80 percent of diagnosed dementia cases. Projections for increasing numbers of Alzheimer’s patients in the coming decades is cause for concern. However, in this digital age where disinformation is in abundance, Right At Home has identified ten persistent myths about Alzheimer’s that should be dispelled for clarity’s sake and because worry increases stress levels, which is bad for the brain.

Myth #1: If I live long enough, I will likely develop Alzheimer’s disease.

The fact is that developing dementia is not a natural function of aging. While there are more diagnosed cases than ever before, and risks increase as we age, it is not inevitable that age equals Alzheimer’s. A University of Michigan poll of people in their 50s and 60s found half the respondents expect to develop serious cognitive and memory loss as they age. The statistics show only twenty percent of older adults will experience dementia.

Myth #2: If I have a genetic predisposition for Alzheimer’s disease, I can do nothing to prevent getting it.

It is a fact that a higher risk for dementia does run in some families. However, research data presented at the July 2019 Alzheimer’s Association International Conference suggest that even those with a higher genetic propensity to develop Alzheimer’s can lower their risk by adopting lifestyle choices that address brain health. Actionable lifestyle choices decreased dementia risks by 32 percent. A study of identical triplets from the University of Toronto (December 2019) revealed while two contracted dementia, the third did not. While there are no guarantees, there are preventable strategies.

Myth #3: If I already have amyloid plaques and neurofibrillary tangles in my brain, I will soon experience Alzheimer’s disease.

Today’s medical technologies like PET scans and other brain imagining techniques show that some people have these plaques and tangles but display no obvious outward disease symptoms. The brain is highly resilient and plastic, creating workarounds or backup connections that bypass the affected brain cells.

Myth #4: Specifically engineered brain games will provide the mental exercise I need to protect against dementia.

Neurologically focused computer games, puzzles, and similar brain “training” products are somewhat useful. Still, they do not provide a greater benefit than other mind-challenging activities. You are just as well off learning a new language, taking an art class, reading, playing video games, traveling, or even working at a mentally stimulating job. These activities help the brain build new connections; in particular, learning something new is especially beneficial.

Myth #5: All I need is solitary brain exercise.

The fact is that while engaging in intense mental focus is great, interacting with other people is more beneficial. Socialization stimulates many more regions of the brain, and those who regularly engage in social activity consistently have a lower incidence of dementia. Staying connected, even virtually in this age of social distancing, also prevents becoming part of the epidemic of loneliness, which leads to many negative health consequences. There are many reasons to stay socially engaged.

Myth #6: Skipping physical exercise is permissible as long as I get mental exercise.

It is a fact that brain stimulation matters, but it is also a fact that exercising our muscles is as important for brain health because the two work together. Physical movement requires brain and muscle memory. Whether you move about a park or a gym, you need to know where to go. You also must know what to do, how to complete each task, and move to the next. In this multi-tasking body/brain exercise work, each function enhances the other—muscles matter.

Myth #7: Only aerobic exercise benefits the brain.

Muscle-strengthening activities are as important as aerobic exercise. It is true that having an aerobically fit heart is good for a healthy brain but lifting weights, doing squats, planks, pushups, and working with resistance bands are all known to boost memory. In some instances, strength training can even reverse memory loss because building muscle makes us overall healthier, and it also increases several beneficial chemicals in the brain.

Myth #8: I can take supplements to protect my brain health.

The fact is you are better off eating a diet that includes lots of quality vegetables and fruits, grains, poultry and fish, and healthy fats like olive oil. America is overrun with vitamins, herbs, and promises of brain health substances. The World Health Organization has recently stated no reputable study confirms the value of these vitamins, herbs, or supplements. Save your money and talk to your doctor about a healthy diet instead.

Myth #9: Drinking alcohol protects my brain.

The fact is experts do not agree about the studies associated with moderate drinking, in particular red wine, with brain health. However, the experts all do agree that drinking too much is very harmful to the brain. Heavy drinking shrinks the brain. The Lancet Public Health Journey states that “alcohol disorders are the most important preventable risk factors for all types of dementia.” As part of your diet plan, talk to your doctor about a safe amount of alcohol for you.

Myth #10: Alzheimer’s disease is not related to other health conditions.

No disease is unrelated to other health conditions in our bodies. Many chronic conditions and diseases can harm our brains like high cholesterol, high blood pressure, diabetes, depression, stress, insomnia, hearing and vision loss, and even gum disease raise the risk of Alzheimer’s. Regular healthcare that manages existing conditions can also lower the risk of memory loss or slow its progression. Routine medical appointments, taking medications as prescribed, and following doctor recommendations can help to preserve brain health.

If you or a loved one have been diagnosed with Alzheimer’s, now is the time to plan. We can help create a comprehensive legal plan to address how to pay for care without losing everything you’ve saved over the years. We would be happy to talk to you about ways we can help. Please contact our New York Office or call us at (212) 937-84

Around the United States, there is a new refrain spoken by Medicare home health providers, including occupational, speech, and physical therapists, social services, as well as intermittent skilled nurses: “Your husband (or whomever) is not going to get better, so we will have to discontinue our services as Medicare will not pay for it.” Termination of care is swift, often within 48 hours of delivering the message, and the home health care chores fall to the family system or must be paid for out of family funds. So what changed?

Significant changes began on January 1, 2020, as to how Medicare pays for home health services. Medicare has altered its billing approach from a therapy delivered model (the more therapy you receive, the higher the payments billed to Medicare) and changed it into a reimbursement system known as the Patient-Driven Groupings Model, or PDGM. Medicare Advantage plans have separate rules and are not affected.

The Centers for Medicare and Medicaid Services (CMS) provide Figure 1 as an example of how a 30 day period becomes categorized into 432 case-mixed groups for adjusting payment purchases in the PDGM. These 30 day periods are further broken into the following subgroups: admission sources and timing, twelve clinical principal diagnosis subgroups, three functional impairment levels, and three levels of co-morbidity adjustments. During the 30 days, there is only an allowance for one chosen category under the larger color-coded categories. CMS deems this newer approach to be more holistic regarding patient need assessments.

In 2017, the most recent year for which the data is available, for-profit US home health care agencies (approximately 12,000) provided care to 3.4 million Medicare beneficiaries. Home health rates charged were based on the amount of therapy delivered. The more therapy a patient received, the higher the payout to the agency. Due to the change in payment structure, these agencies are cutting back on therapies provided and even reducing the number of therapists employed. They can’t bill enough to Medicare to remain profitable. These new payment conditions are based on a patient’s underlying diagnosis and other case-specific complicating medical factors. As a result, home health care agencies now have a stronger financial incentive to meet the needs of short-term therapy, post-hospital or rehab facility, as well as caring for patients requiring nursing care for complex situations like post-surgical wounds.

CMS believes this new way to assess payments will strike a balance between costs, efficiencies, needs, and outcomes. The members of the National Association for Home Care and Hospice (NAHC) disagree. Data culled by NAHC from home health agencies indicate there will be a substantial reduction of therapy services offered as a result of the PDGM. William Dombi, the association’s president, states that the cuts “may not be a good move” because medically, patients may deteriorate more rapidly without therapy and seek aid in emergency rooms or hospitals. He also notes the possibility that if more patients end up worse off and go to emergency rooms or hospitals, that this will reflect poorly on home health agencies and can affect their referrals.

Providing the right patient therapy at the right time by home health care agencies is critical to positive patient outcomes. CMS has done extensive analysis of historical data and, through the use of artificial intelligence tools, feel they can better predict what kind of services and how often a patient will need them through the PDGM. Clarifications are being posted online by CMS that deal with early errors in the program and the ensuing turmoil of therapy provision for patients within the new guidelines. It is the hope that more reviews and revisions to the PDGM will strike a better balance between cost and efficiency, patient therapy needs, and outcomes.

Understanding the role Medicare will play when it comes to long term care services can be confusing. We help families plan for the possibility of needing long term care, and how it could be paid for without causing the family to spend everything they have.

If you have questions or would like to discuss a personal legal matter, don’t hesitate to reach out. Please contact our New York office or call at (212) 937-8420.

Wills and trusts have specific and quite different benefits for estate planning purposes. Each state has specific laws and regulations governing these legal documents. You can have both a will and a trust; however, the information in each should compliment the other. As a standalone, it is not accurate to say one is better than the other. The better choice for you, or a blend of both documents, depends on your assets and life circumstances. Begin by assessing your situation, goals, and needs, and understanding what wills and trusts do to guide your decision making. Then, along with an attorney, you will be able to identify the solution that best suits and protects your family.

At its most basic level, a will allows you to appoint an executor for your estate, name guardians for your children and pets, designate where your assets go, and specify final wishes and arrangements. A will is only enacted upon your death. It has some limitations regarding the distribution of assets, and wills are also subject to a probate process (which occurs in court and is overseen by a judge) and, as such, are part of public records.

The last will and testament designates a person’s final wishes about bank accounts, real estate, personal property, and who should inherit these items. A personal will outlines how to distribute possessions, whether to another person, a group, or donate them to charity. It also deems responsibility to others for custody of dependents and management of accounts and other interests. Accounts can include digital assets with a tangible or monetary value associated with it, such as funds in a PayPal account.

A pour-over will ensures an individual’s remaining assets will automatically transfer to a previously established trust upon their death. This type of will always accompanies a trust.

A living will or advance directive specifies the type of medical care that an individual prefers if they cannot communicate their wishes.

A joint will and mutual will is meant for a married couple to ensure that their property is disposed of in an identical manner. A mirror will is two separate but identical wills, which may or may not also be mutual wills.

A holographic or handwritten will is valid in about half of the states and must meet the specific state’s requirements. Authentication of this will type for acceptance to the probate process also varies by state. There is always the possibility that a court will not accept a holographic will. Even if you have limited assets, your best strategy is to have your will professionally documented by an attorney. A video of your final wishes does not create a valid will.

Trusts are somewhat more complicated than wills, and the many different trust types can greatly benefit your estate and beneficiaries. Generally, a trust provides for the distribution and management of your assets during your lifetime and after death. Trusts can apply to any asset you hold inside the trust and offer more control over when and how your assets are distributed. There are many different trust forms and types, far more than wills.

However, the creation of a trust is only the beginning of the process. You must fund your trust by legally transferring assets into it, making the trust the owner of those assets. This process makes creating a trust a bit more complicated to set up; however, a trust is often enacted to minimize or completely avoid probate, thus keeping personal records private. Avoiding probate is a huge advantage for some people and often justifies the additional complex legal work of setting up a trust. There are nearly as many types of trusts as issues to address in your estate planning, and each offers different protections. However, trusts generally fall into three basic categories.

A revocable living trust is, by far, the most commonly implemented trust type. The person who creates and funds the trust is known as the grantor and will typically act as the directing trustee during their lifetime. The grantor may undo the trust, change its terms, and move property and assets in and out of the trust’s ownership as they deem desirable. Revocable living trusts are designed to switch to an irrevocable trust upon the death of the grantor.

An irrevocable living trust is legally binding on its date of designation and allows very few provisions for change. The trust grantor funds the irrevocable living trust with property and assets, and the trust property is then under the care and control of the individual the grantor names as trustee. The grantor cannot change their mind and “undo” the trust. There are unique tax implications and other benefits to an irrevocable trust, including protecting a person’s home and savings from the high costs of long term care. These benefits can make relinquishing control worthwhile.

A testamentary trust is a provision within a will, appointing a trustee to manage the deceased’s assets. This trust is often used when the beneficiaries are minor children or someone who is receiving public benefits. This trust type is also used to reduce estate tax liabilities and ensure professional asset management. A testamentary trust is not a living trust. It only exists upon the death of the testator (the writer of the will). The executor of the deceased’s estate would follow the terms of the trust (called administering the trust) as part of the probate process.

Successfully addressing and legally formalizing inheritance of family values and assets can be challenging, especially if parents wait too long to begin instilling family values. Undoubtedly the best time to teach and empower your children as eventual inheritors of your family legacy is during childhood, then continuing throughout adulthood. Waiting until your later stages in life to discuss family values as a guide to handling inherited worth is often ill-received as grown adult children prefer not to feel parented anymore, particularly when they are raising children of their own.

There is value in the spiritual, intellectual, and human capital of rising generations, and it is incumbent upon older generations to embrace this notion and work with their heirs rather than dictating to them their ideas about how to facilitate better outcomes. While the directions taken by newer generations will likely differ and can sometimes be downright frightening than that of their elders, there can still be a deep sense of service and responsibility to family values and stewardship of inherited wealth. Allow your children to exert their influence over the family enterprise early on in life and make adjustments that create synergy, connection, and like-mindedness.

If this description of a somewhat ideal family system does not resemble yours, take heart. Most families do not conform to perfect standards of interaction. The more affluent a family is, the higher the failure rate to disperse assets without severe fallout. The Williams Group conducted a 20-year study and determined there is a 70 percent failure rate that includes rapid asset depletion and disintegration of family relationships during and after inheritance. Establishing inheritable trusts can provide real benefits. Benefits include avoiding probate, reducing time to handle estate matters, privacy protection, the elimination or reduction of the estate tax, and can be effective pre-nuptial planning. A parent who wants to control outcomes should focus on these benefits of the trust instead of trying to legislate their future adult children’s behavior.

It is imperative not to allow your values and legacy to become weaponized within the family system. A sure-fire way to inspire conflict is via “dead hand control,” meaning trying to control lives from the grave. Most often, if you put excessive trust restraints on adult children, they will act accordingly to your perception that they are not adult enough to handle wealth. Instead, consider enrolling them in a few classes about managing wealth. Spark an interest in them to learn how you have created wealth, the mechanisms you used, and what their future endeavors may look like long after you are gone. Formally educate your children about finances, the earlier the better, and instead of talking about who gets what the conversation can shift to the mechanics of managing wealth. This tactic resets the context of the issue and aligns purpose and intended long term outcomes.

Estate planners try to encourage trust choices that lead to flexibility. If a beneficiary is genuinely incapable of making the right decisions, a trustee can be appointed to make distributions in the beneficiary’s best interest. This trustee discretionary power of money management can help a well-funded trust survive for generations.

You can also write a letter of wishes or provide a statement of intent to your children. Though these are not legally binding, it gives you a platform to remind them of family values and your desire for these values to be maintained for future family generations. This type of letter is an opportunity for you to convey your vision for how your wealth can bring growth and chance for fulfillment to beneficiaries.

Prosperity should positively shape lives. Family trust beneficiaries hopefully already have a self-driven life that includes purpose, responsible behavior, and a basic understanding of personal finance. If you worry your children may squander inheritable assets, create the opportunity for them to succeed through classes that teach them about managing legacy family values and wealth. Address your concerns legally and directly through a detailed trust that can help but not overly constrain them to achieve what you envision they can become. Start an honest conversation early on, but remember it is never too late to make good choices and create positive family value influences for the coming generations. A well-known Ann Landers quote sums it up neatly, “In the final analysis it is not what you do for your children but what you have taught them to do for themselves that will make them successful human beings” – a worthy goal of any family value system.

If you are interested in establishing a trust to pass wealth on to your children, we can help. We can also guide families on how to pass on family values in a meaningful way. We look forward to the opportunity to work with you.

Whether you are starting from scratch or have an estate plan in place a letter of instruction (LOI) is an important part of any comprehensive plan. A letter of instruction can help your loved ones manage important information about you. A LOI conveys your desires, includes practical information about where to find various items referenced in your plan, and it can provide advice to help those you designate in managing your affairs.

Even with a new or updated estate plan, there exists a lot of information that your heirs need to know that doesn’t necessarily fit into the format of a will, trust, or other estate plan components. In the absence of this information, it is easy for those in charge to miss important items and alternatively become overwhelmed, sifting through all of the documents you left behind. All LOI’s are as different as the persons who wrote them; however, there are some standard data that every LOI should include:

A note about your digital footprint: your digital world often includes music libraries, storefronts, YouTube channels, influencer social media accounts, etc. When most of us create these accounts, we blithely accepted the End User License Agreement (EULA) without much thought about when we are no longer around to manage its content and activity. A EULA designates the rights and restrictions that apply when using the software known as terms of service (TOS). Naming someone capable of managing your digital-assets and their activity is important. Most of your online accounts are not subject to typical estates planning devices like trusts and wills because they are not technically your property. Since most TOS are non-transferable, you will be unable to transfer your online accounts’ ownership legally. However, you can still make a plan for how they are handled when you die.

Once you write your letter, put it somewhere easily accessible and tell your family about it. If you do not want anyone to read the LOI until your death, seal it in an envelope. You should review your letter once a year to be sure it reflects your most current wishes and information. Because your heirs read your letter of intent upon your death, it can be difficult for you to write and have any degree of satisfaction. Final words and conveyances are sobering.

We can help you compose such a letter (as well as other estate planning documents), making sure that it compliments and does not contradict your estate plan. Remember that your LOI can bring real peace and be a source of comfort to your grieving family members. It allows them time to contemplate and connect with others to celebrate you rather than sort through documents searching for important papers. Your LOI can also alleviate potential family conflicts and stress because you specifically address personal items’ distribution. Your goal should be to ease the burden for those in charge and gain a sense of peace that you have done all you can to allow your loved ones to focus on reflecting on your life.

When you are ready to take the next step, we will be here to help.